"There are decades where nothing happens, and there are weeks where decades happen."

From tensions in the Middle East, through unprecedented political shifts in East Asia, border clashes happening across the globe, to an increasingly dire situation in the Ukraine — it became clear very quickly that 2026 will be made out of weeks holding a decade's worth of events. On top of all the political and geopolitical uncertainties, 2026 seems to be a year where steps towards AGI turn into jumps. New AI models are released constantly, each a significant improvement over the last, and each seemingly targeting a different industry. This uncertainty is felt in the media as well as the markets, with safe-haven assets rallying in tandem with the uncertainty index VIX.

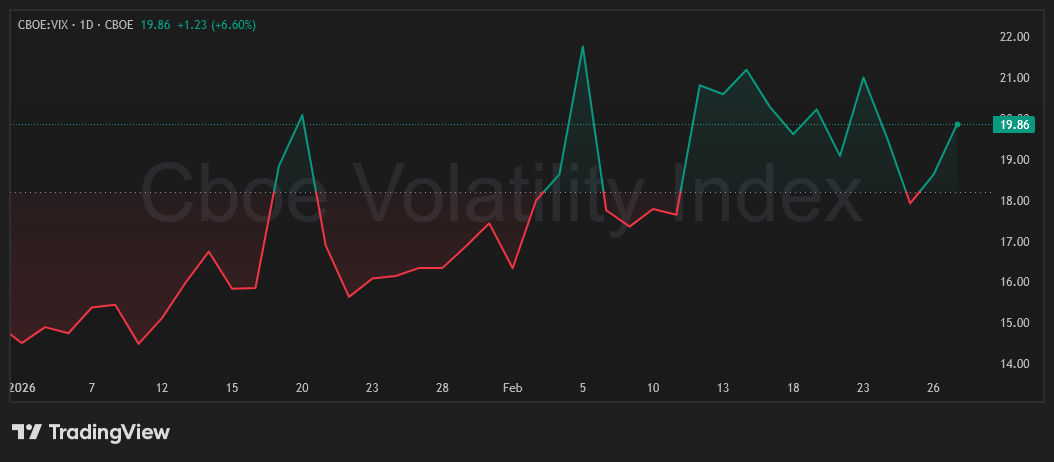

The CBOE Volatility Index (VIX) rallied by almost 25% since the start of 2026 until the final trading session in February. Source: Godel Terminal via Trading View.

Every new press release from OpenAI or Anthropic seems to send tremors across the market, causing sell offs of some of the largest names in the technology sector, like Cloudflare or IBM. Investors seem to price in the AI disruptions with rapid fire speed, every new feature taking tens of per cents from companies' market caps. Among this uncertainty, the hyperscalers are pledging record sums to be invested into their compute capacity, to build and maintain data centres and support higher degree of AI adoption. In late 2025 Goldman Sachs forecasted ~500 billion USD to be spent on this. In early 2026 big tech has already pledged north of 650 billion USD as their 2026 AI capital expenditures. Their profits have been growing, but nowhere near as fast as their AI spending, which already has many economists and analysts questioning how sustainable this model is. Many, like Michael Burry, are taking a closer look at the circular deals between AI companies, which seem to move billions just to end up with the same amount of cash they held before. More voices, like Ray Dalio (Bridgewater Associates) or Steven Druckenmiller (Quantum Fund), are raising concerns about an AI bubble — a term which would get you ostracised in early 2025, and pointing to the ballooned-up valuations of technological companies.

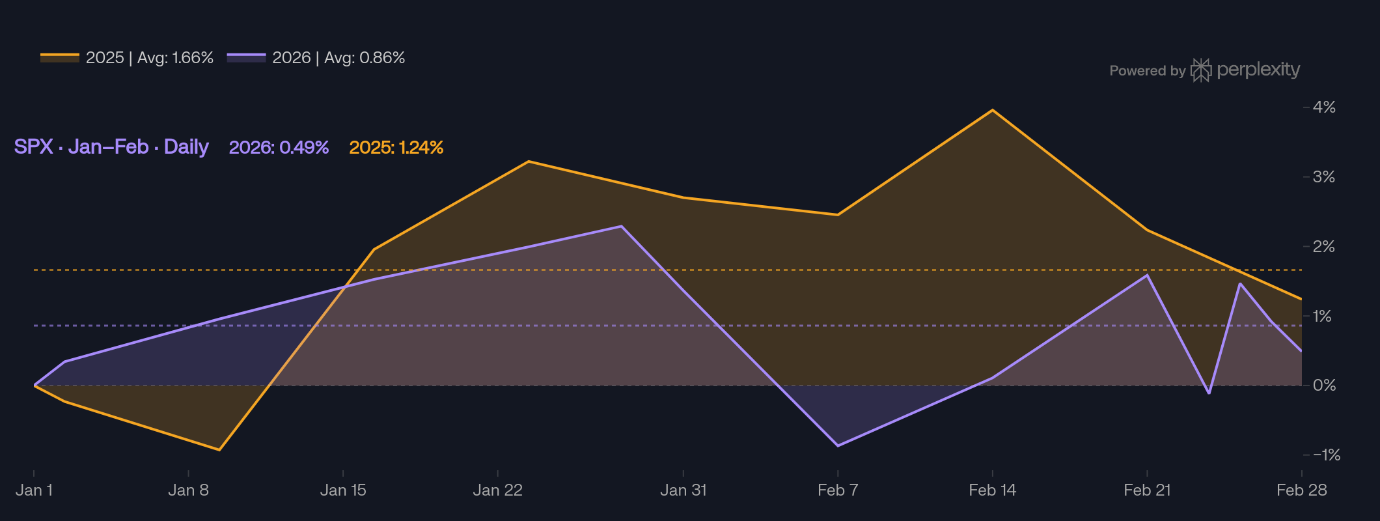

The S&P 500 index (SPX) returns in the first two months of 2025 (orange) and 2026 (violet) expressed in %. Despite the uncertainty around the policies of Trump 2.0, sworn in on the 20th of January 2025, the average return for the two months was 1.66%, almost double the average return for 2026 in the equivalent period.

The market is volatile, the development of AI unprecedented, the fears of AI-induced mass lay-offs greater than ever before. This is the scene unto which, on Sunday the 22nd of February, a report titled "The 2028 Global Intelligence Crisis" is released by Citrini Research, a market research outlet, together with Alap Shah, the CIO of the Lotus Technology Management fund. Their thought experiment offers a new take on the AI induced recession and crash. Usually the question asked is "what if revenues don't match the AI spending?" Citrini takes the opposite side of that worry: what if AI is too good at what it's supposed to do — boosting productivity? The rise of agentic AI puts a lot of white-collar jobs at risk. Agents specialising in coding (Codex) or financial accounting (Claude Financial Analysis Solutions) are popping up more often, and innovations like Open-Claw seem to democratise automatization. Implementing AI allows companies to increase their margins by reducing their headcount. At first, argues Citrini, the AI rally commences, as productivity and earnings grow. AI gets implemented more, there is more training data, it gets better at more tasks and gets implemented into more fields. In pursuit of margins, headcounts are constantly reduced. Revenue per employee skyrockets, but so does unemployment. As AI gets implemented more, it optimizes more, reducing the elements of brand loyalty, as AI agents acting as shoppers communicate with AI agents in the role of sellers, without the human error or preference. Jobs are lost, spending cools. To combat this, companies employ more AI tools and cut costs via lay-offs, creating a death spiral. Citrini goes a step further, predicting this will only be the start of the actual crisis. Next domino to fall will be the credit market, beginning with mortgages and defaults on loans given to software companies. Citrini predicts the AI disruption of all white-collar work to come by very fast, and force unprepared lenders to face mass defaults.

Despite the Citrini report being clearly advertised and described as a thought experiment and, thus, a thought-provoking fiction, the markets reacted as if Citrini had a glass ball and told the future. All companies named in the article saw sell-offs on Monday, the first trading day after publication. Companies as large as KKR & Co, Uber, Visa, Blackstone, or Apollo Wealth Management saw their shares slump, caught up in the "AI scare trade." The report seems to embody much of what those pessimistic about AI already think, it just puts it all in one well put together article. But, as it usually is the case with forecasting the future, Citrini's viewpoint is highly contested by many from independent analysts to the famously secretive hedge fund Citadel Securities.

Most, if not all, of the stocks mentioned in the Citrini report opened lower on Monday the 23rd, following the report's release, and continued to slump as the session progressed. At the same time the S&P and NASDAQ Composite indices dropped 1% and 1.1% respectively in the same session.

In response to Citrini, Citadel's macro strategist Frank Flight explains why he believes the scale of disruption described is unlikely. First, he argues, replacing white-collar workers at that scale would require massive amounts of costly compute. Of course, as AI implementation progresses, we can expect the price of compute to drop, but not fast enough to justify replacing most human labour with AI, as the cost of running those models would surpass the cost of human capital — directly going against Citrini's margin-expanding paradigm. Coding jobs are those, which everyone seems to agree will be the first ones replaced by AI. But Flight showed that Indeed postings for coding and programming jobs have increased in recent months. The demand for data centres has also caused an increase in job openings in construction — which shows one of the potential mechanisms through which AI adoption may shift the need for employees, rather than removing it completely. Finally, Flight argues that recursive technology, like AI working to improve itself, is not adopted recursively. The adoption speed slows down significantly as the market gets saturated. And for the spike in adoption to cause layoffs like those envisioned by Citrini, the speed at which AI replaces jobs would not only need to be quicker than its potential to create new jobs but would also have to be met with "no fiscal response, negligible investment absorption, and unconstrained scaling of compute."

Another point which is important to mention as it can significantly impact the credibility of Citrini's research and forecasting capacity, is the fact that his co-author, Alap Shah, is the CIO of a fund, which, prior to the release of the report, "certainly had shorts in some of these [mentioned in the report] businesses" as well as "generally having a set of shorts out against businesses [they] think are going to be disrupted by AI." Not enough information is available to accuse Citrini of producing a Hindenburg Research-esque short seller report, but there is certainly enough to raise caution.

Citrini's thought experiment came out at a time when markets and investors are biting their nails, waiting for the next market-breaking news to come out. Among the geopolitical tensions, threats of war (now realised, at a time of writing this article), and the human fear of the unknown, it is no wonder why putting forward the thesis that Citrini's James van Geelen grabbed the spotlight and peaked interest. But the overblown response to it may be more telling than the report itself. It showed how unnerved both institutional and retail investors are, and how little it takes to move billions. The unhealthy state of the markets, despite GDP growth, jobs being added quarterly, productivity increasing should be worrying. It shows that despite already seeming off, things may be even worse than they seem.

Main Readings

- Van Geelen, J. and Shah, A. (2026) The 2028 Global Intelligence Crisis. Citrini Research, 22 February. https://www.citriniresearch.com/p/2028gic

- Flight, F. (2026) 2026 global intelligence crisis. Citadel Securities Macro Strategy Report, 26 February. https://www.citadelsecurities.com/news-and-insights/2026-global-intelligence-crisis/

Further Readings

- Manidis, W. (2026) 'On the garden (against Citrini)', Minutes [Substack], 23 February. https://open.substack.com/pub/minutes/p/on-the-garden-against-citrini

- Goldman Sachs (2025) Why AI companies may invest more than $500 billion in 2026. Goldman Sachs Insights, 17 December.